Market Overview

| Study Period | 2021 - 2031 |

|---|---|

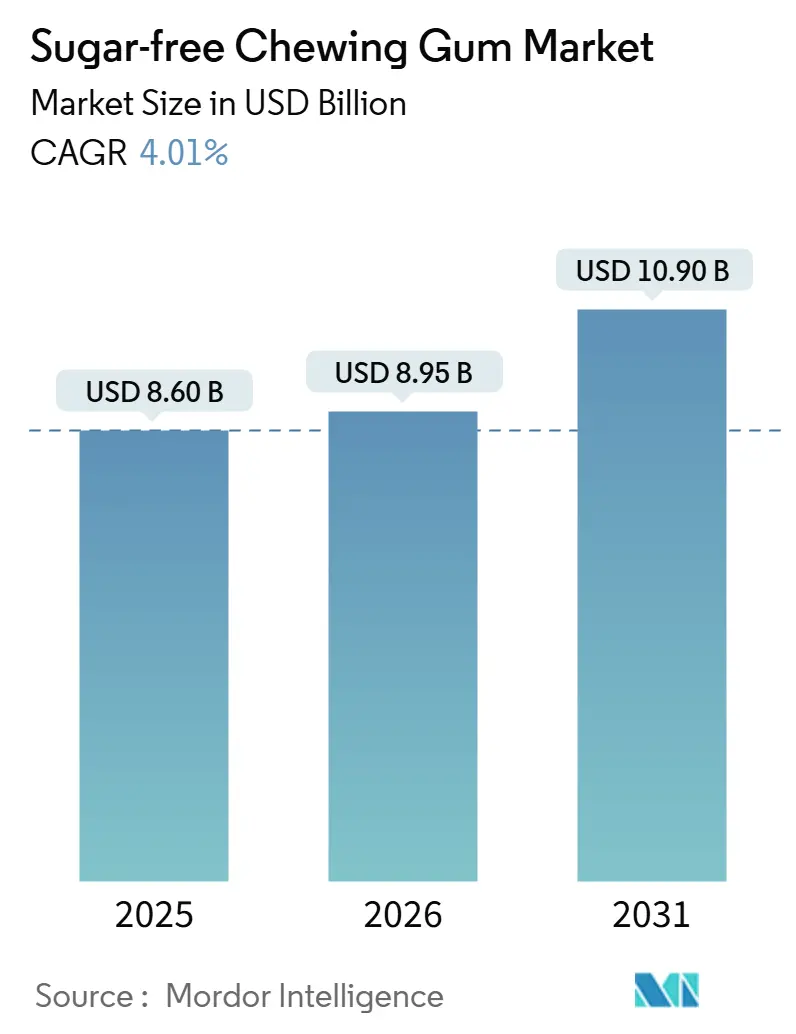

| Market Size (2026) | USD 8.95 Billion |

| Market Size (2031) | USD 10.90 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

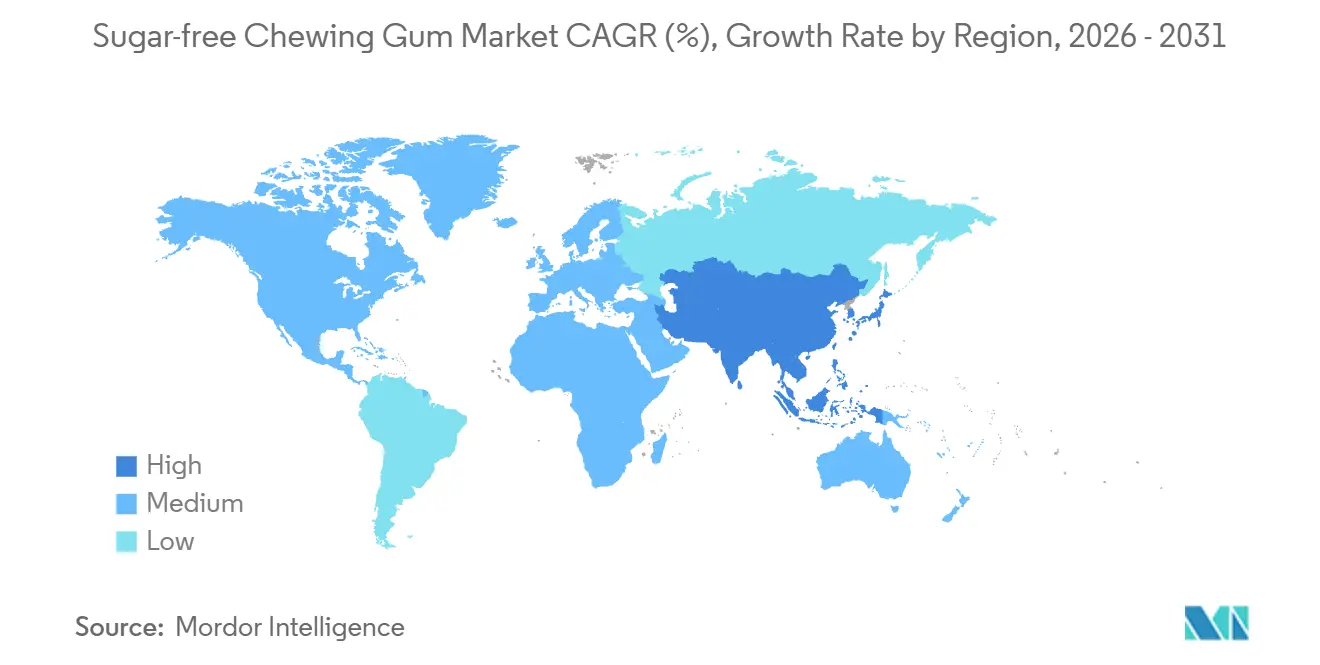

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sugar-free Chewing Gum Market Analysis by Mordor Intelligence

The sugar free chewing gum market size was valued at USD 8.60 billion in 2025 and estimated to grow from USD 8.95 billion in 2026 to reach USD 10.90 billion by 2031, at a CAGR of 4.01% during the forecast period (2026-2031). Purpose-driven flavor research, soft-chew texture engineering, and clean-label reformulations are now more influential than simple volume expansion in shaping competitive advantage. Artificial sweeteners still dominate formulation cost structures, yet natural alternatives are capturing mind-share as polyol and stevia suppliers improve taste profiles. Soft-chew and cube formats are winning incremental facings because they satisfy snacking occasions that traditional stick gum cannot reach. Direct-to-consumer subscription packs continue to pressure checkout-lane sales by making replenishment frictionless, while function-forward launches—caffeine, probiotics, hydroxyapatite—broaden usage into stress relief, concentration, and oral‐care routines. Meanwhile, color-antagonistic reformulations announced by large incumbents underline that compliance now requires continuous agility rather than episodic updates.

Key Report Takeaways

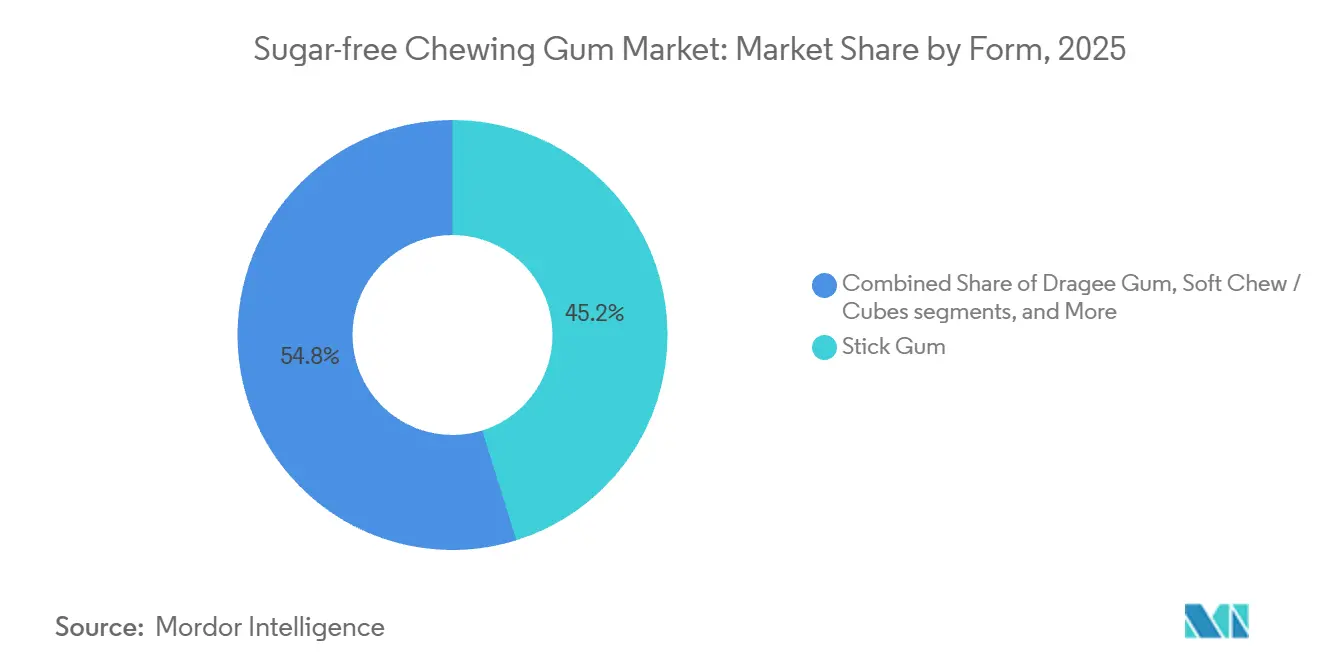

- By form, stick gum led with 45.20% revenue share in 2025; soft-chew and cube formats are projected to expand at a 4.27% CAGR to 2031.

- By sweetener type, artificial sweeteners commanded 70.7% of 2025 revenue, while natural sweeteners are forecast to grow at a 5.01% CAGR through 2031.

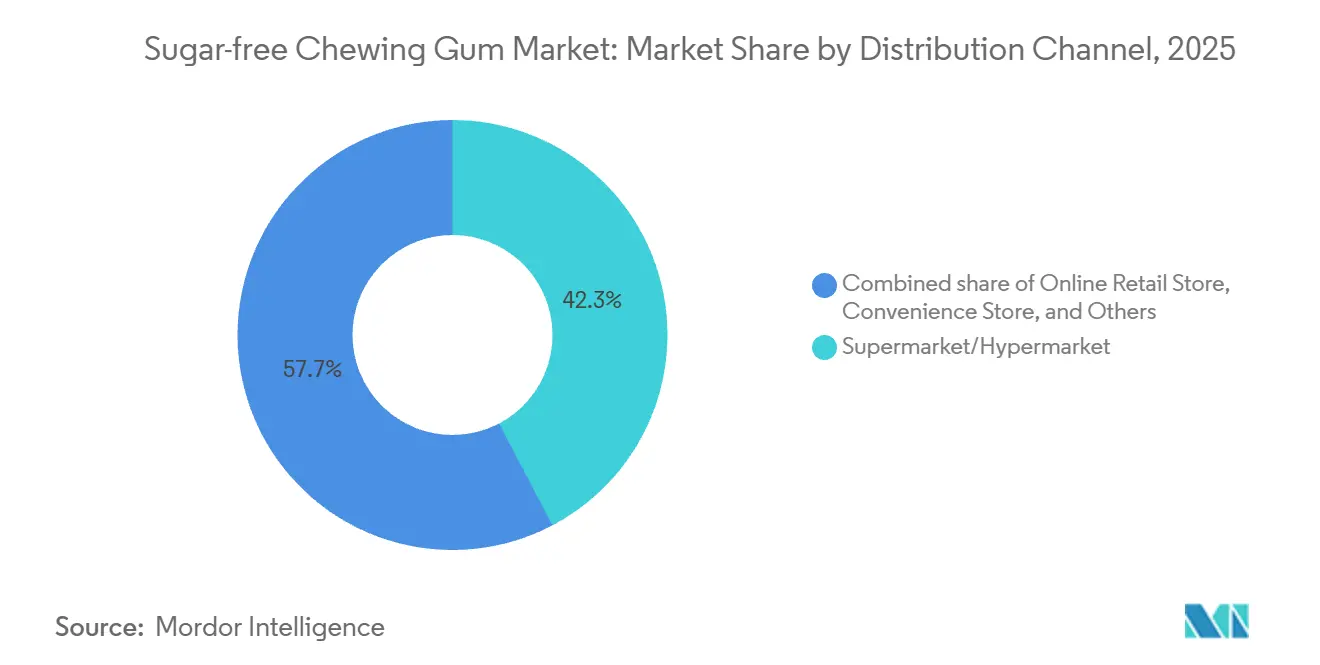

- By distribution channel, supermarkets and hypermarkets captured 42.3% of 2025 sales; online retail is forecast to rise at a 5.67% CAGR to 2031.

- North America accounted for 41.8% of 2025 revenue, yet Asia-Pacific is expected to register the fastest regional CAGR at 5.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sugar-free Chewing Gum Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-the-go and discreet use across daily routines | +0.8% | Global, with strongest uptake in North America, Western Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Flavor and Format Innovation | +1.1% | Global, with early adoption in North America and Japan; spill-over to emerging markets | Medium term (2-4 years) |

| Oral Health Positioning and Dental Endorsements | +0.9% | North America, Europe, Australia; emerging in India and Southeast Asia | Medium term (2-4 years) |

| Smoking-cessation and Behavioural Health Trends Driving Growth | +0.5% | North America, Europe; limited penetration in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Personalization and Segmented Propositions | +0.4% | North America, Western Europe; nascent in Asia-Pacific | Long term (≥ 4 years) |

| Clean-Label and Natural Cues Driving Growth | +1.2% | Global, with premium positioning in North America, Europe; value positioning in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Flavor and Format Innovation

Flavor-changing and texture-enhancing technologies are transforming consumer expectations and boosting product turnover on shelves. In September 2024, Hershey introduced Ice Breakers Flavor Shifters, a pellet gum that changes flavors during chewing. This innovation uses encapsulation chemistry to control the release of flavors, extending the sensation of freshness. Similarly, in July 2024, Mars Wrigley launched EXCEL Refreshers in Canada. These soft-chew gums combine fruity flavors with cooling agents, targeting millennials who perceive traditional stick gum as outdated. Perfetti Van Melle released Trident Vibes Cotton Candy in May 2025, priced at USD 3.84 per bottle. This product highlights how nostalgic flavors paired with sugar-free formulations can attract premium pricing in convenience stores. In the same month, Mondelez announced its efforts to develop controlled-release flavor technology that could sustain taste for 30 minutes. If successful, this would surpass the current 10-to-15-minute standard and redefine competition in the market. Soft chew and cube gum formats are projected to grow at a 4.27% CAGR through 2031, outperforming the slower growth of stick gum. These formats are gaining popularity due to their higher perceived value per piece and their suitability for snacking occasions beyond just freshening breath.

Oral Health Positioning and Dental Endorsements

Sugar-free gum has evolved from a niche product for caries prevention to a mainstream oral health tool, with its adoption influenced by regulatory frameworks and professional endorsements. The American Dental Association highlights the benefits of xylitol and polyol sweeteners, which stimulate saliva production and reduce plaque pH, providing a strong scientific foundation for brands like Orbit and Trident to promote these benefits in their marketing. In Japan, Lotte's Xylitol Oratect Gum, containing 6.0 grams of xylitol and 0.48 milligrams of eucalyptus extract per 10 tablets, holds a special health-food designation from the Consumer Affairs Agency. This designation allows it to claim gum-health benefits that standard products cannot. In the UK, the Oral Health Foundation endorses Peppersmith's 100% xylitol gum, supporting its premium pricing of GBP 15.99 to GBP 19.99 for multi-packs, nearly double the cost of aspartame-based alternatives. In January 2024, Mars Wrigley rebranded its Orbit, Extra, Freedent, and Yida products under the "Chew You Good" campaign. This strategic shift positions gum as a wellness product rather than a confectionery item, aligning with the increasing demand for low-calorie, hydrating snacks driven by the rising adoption of GLP-1 medications and health-conscious consumer trends.

Smoking-cessation and Behavioural Health Trends Driving Growth

Functional gums aimed at smoking cessation, stress relief, and cognitive enhancement are gaining traction as high-margin products, leveraging sugar-free formulations for delivery. Nicotine gum, endorsed by the Truth Initiative as a first-line treatment for tobacco cessation, has set a precedent for the credibility of non-nicotine functional gums. The CDC recognizes nicotine gum as a critical tool in helping individuals quit smoking. Research indicates that using 4 mg nicotine gum alongside behavioral counseling can double the likelihood of quitting compared to a placebo. The U.S. Surgeon General's 2024 report highlights over-the-counter nicotine gum as an affordable and accessible solution, particularly benefiting low-income populations who may not have access to prescription treatments. This shift has also normalized gum chewing in professional settings, transforming it into a health-conscious habit. Brands like NeuroGum and REV GUM have capitalized on this trend by introducing sugar-free gums infused with caffeine, L-theanine, and B-vitamins, marketed to enhance focus and productivity at work. Furthermore, the American Academy of Pediatric Dentistry's 2024 endorsement of xylitol gum for children emphasizes its role in preventive health. This recognition has expanded gum's utility, making it a valuable addition to family health routines and not just a tool for adult smokers[1]Source: American Academy of Pediatric Dentistry. "Policy on the Use of Xylitol", aapd.org..

Clean-Label and Natural Cues Driving Growth

Natural sweeteners are expected to grow at a 5.01% CAGR through 2031, outpacing the 4.01% growth rate of artificial sweeteners. This growth is driven by consumers prioritizing ingredient transparency and allergen-free products. According to an April 2024 IFIC Foundation survey, 30% of U.S. consumers avoid low- and no-calorie sweeteners due to safety concerns and a preference for "natural" options[2]Source: IFIC Foundation. "2024 Food and Health Survey." foodinsight.org.. Among sweetener users, stevia ranked highest in preference, scoring 4.8 out of 10, ahead of aspartame and sucralose. Simply Gum, which uses a chicle gum base and xylitol, sells 6-packs at USD 17.99, a 60% premium over mass-market options. Its focus on natural formulations has driven direct-to-consumer growth. PUR Company reported an 80.6% increase in U.S. sales, reaching USD 8.6 million in the 52 weeks ending May 2025. This growth is attributed to its 100% xylitol formula, vegan certification, and absence of soy, gluten, and artificial flavors, appealing to health-conscious millennials and parents. Peppersmith markets its gum as "made with real ingredients," using British peppermint oil, priced at GBP 15.99 to GBP 19.99, and endorsed by the Oral Health Foundation. Mars Wrigley announced in July 2025 that its Extra Gum Spearmint will exclude FD&C colors by 2026, reflecting the shift toward natural products as a mainstream expectation.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Skepticism Toward Artificial Sweeteners | -0.7% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Regulatory and Labeling Complexity | -0.3% | Global, with highest compliance burden in EU, North America, and Australia | Long term (≥ 4 years) |

| Price Sensitivity and Premium Positioning of Sugar-Free/Formulated SKUs | -0.6% | Asia-Pacific, Latin America, Middle East & Africa; moderate in North America value channels | Short term (≤ 2 years) |

| Supply Chain and Ingredient Risks for Specific Sweeteners, Flavors, and Gum Bases | -0.4% | Global, with acute exposure in xylitol (China sourcing), stevia (South America), and chicle (Central America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Skepticism Toward Artificial Sweeteners

In 2024, the World Health Organization (WHO) designated aspartame as a Group 2B carcinogen, indicating it is "possibly carcinogenic to humans" based on limited evidence. This declaration has reignited consumer apprehensions regarding artificial sweeteners. Nevertheless, the Joint FAO/WHO Expert Committee on Food Additives has reiterated that an acceptable daily intake of 40 mg/kg body weight is still deemed safe. The WHO's announcement, amplified by social media, has widened the chasm between public sentiment and regulatory reassurances. While entities like the FDA and EFSA persist in endorsing aspartame's safety at sanctioned levels, surveys from late 2024 reveal a 22% dip in consumer inclination to purchase products where aspartame is the primary sweetener[3]Source: U.S. Food and Drug Administration. "High-Intensity Sweeteners", fda.gov. . This change has hit legacy brands, long dependent on aspartame for its cost-effectiveness and clean flavor. In response, these brands are reformulating with alternatives such as stevia, monk fruit, or erythritol, leading to a 15-25% surge in ingredient costs. Conversely, smaller entities like The PUR Company are capitalizing on the situation, marketing "aspartame-free" products as a primary selling point and using the regulatory ambiguity to challenge larger competitors.

Price Sensitivity and Premium Positioning of Sugar-Free/Formulated SKUs

Sugar-free gum is priced higher than regular gum due to factors like sweetener type and brand positioning, with price sensitivity varying across regions and retail channels. In the United States, premium and natural-positioned brands are significantly more expensive than mass-market options, limiting their appeal to higher-income urban consumers. On the other hand, markets with a strong focus on value-for-money prefer affordable sugar-free options over premium products with natural sweeteners. In China, the growing popularity of discount retail formats and value-driven shopping habits is reshaping the market, making affordability a key factor in product selection. Similarly, in India, sugar-free gum is positioned as a premium product in a price-sensitive confectionery market, appealing mainly to urban middle-class consumers. In mature markets like the United States, limited retail shelf space is allocated to high-turnover products, creating challenges for premium sugar-free brands without strong promotional support. To address price resistance, emerging players are focusing on functional benefits such as cognitive support, oral health, and probiotics. This approach helps justify higher prices by offering tangible benefits and expands usage occasions beyond breath freshening. These strategies are reshaping the sugar-free gum market, catering to evolving consumer preferences and regional dynamics.

Segment Analysis

By Form: Soft Chew Gains as Stick Gum Matures

In 2025, stick gum held a 45.20% market share, reflecting its long-standing popularity and consumer trust. However, its mature position limits innovation. Mars Wrigley's Orbit and Extra brands generated USD 1.7 billion in U.S. sugarless gum sales by May 2025, primarily relying on stick formats. To adapt, Mars launched EXCEL Refreshers in Canada in July 2024, a soft-chew gum combining fruity flavors with cooling agents, signaling a shift toward texture innovation. Stick gum remains favored for its portability and discreet use, especially in offices and during commutes. However, reduced front-end retail space forces brands to justify each SKU with higher margins or strategic relevance, challenging low-performing stick variants. Dragee gum, tablets, and other formats are gaining traction, with dragee formats particularly popular in Europe and Asia-Pacific due to resealable packaging and premium appeal.

Soft chew and cube formats are projected to grow at a 4.27% CAGR through 2031, driven by younger consumers seeking diverse textures and intense flavors. Perfetti Van Melle introduced Trident Vibes Cotton Candy in May 2025 at USD 3.84 per bottle, offering nostalgic flavors in a soft-chew format. Mars Wrigley launched Orbit White in 2024, targeting consumers who prefer snackable textures over traditional stick gum. Hershey's Ice Breakers Flavor Shifters, launched in September 2024, uses pellet technology for sequential flavor release, a feature stick gum cannot offer. Mondelez, in May 2025, announced efforts to develop controlled-release flavor technology for soft-chew gum, aiming to extend taste duration to 30 minutes, surpassing current standards. This shift highlights the category's evolution from functional breath-freshening to experiential snacking, expanding usage occasions and supporting premium pricing.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sweetener Type: Natural Gains Despite Artificial Dominance

In 2025, artificial sweeteners dominated the market with a 70.7% share, supported by long-standing regulatory approvals, cost-effectiveness, and their ability to mask taste. However, natural sweeteners are projected to grow at a 5.01% CAGR through 2031, reflecting a shift toward clean-label products. Popular brands like Mars Wrigley's Extra and Orbit rely on artificial sweeteners such as aspartame, sucralose, and acesulfame-K, benefiting from economies of scale and efficient supply chains to maintain competitive pricing. Regulatory stability remains strong, with the U.S. FDA approving six high-intensity sweeteners and the European Food Safety Authority reaffirming safe intake levels for acesulfame-K and steviol glycosides in 2024. However, the World Health Organization’s caution against non-sugar sweeteners for weight management, excluding polyols, has raised questions about their health benefits. Premium brands are leveraging this uncertainty by focusing on dental health benefits rather than calorie reduction.

Natural sweeteners like xylitol, stevia, and erythritol are gaining traction due to consumer demand for transparent and allergen-free ingredients. An April 2024 IFIC Foundation survey showed stevia as the most preferred low-calorie sweetener, scoring 4.8 out of 10, ahead of aspartame and sucralose. Brands like Simply Gum and Peppersmith capitalize on this trend by offering natural formulations at premium prices, while Lotte’s Xylitol Oratect Gum in Japan highlights gum-health benefits. This has created a two-tier market, with mass-market brands focusing on volume and premium brands targeting higher margins. As natural sweetener supply increases and costs decrease, this divide is expected to grow further.

By Distribution Channel: Online Retail Disrupts Front-End Dominance

In 2025, supermarkets and hypermarkets accounted for 42.3% of the distribution share, reflecting their long-standing dominance in front-end placements and checkout lanes. However, these channels face challenges as retailers focus on optimizing space and prioritizing fast-moving SKUs. Mars Wrigley achieved an 8.1% year-over-year growth, primarily through supermarkets and hypermarkets, by utilizing promotional budgets and securing shelf-space agreements that smaller brands struggle to match. Perfetti Van Melle, after acquiring Mondelez's developed-market gum business for USD 1.35 billion in 2023, gained access to Trident and Dentyne’s supermarket networks. This acquisition resulted in USD 849.8 million in U.S. sugarless gum sales for the 52 weeks ending May 2025, despite a 4.3% decline due to reduced SKU counts. Convenience stores hold a significant share, especially in Asia-Pacific and North America, driven by on-the-go consumption and single-serve packaging. Other channels, such as vending machines and specialty retail, make up the remaining market share.

Online retail is expected to grow at a 5.67% CAGR through 2031, driven by direct-to-consumer brands using subscription models and social media to bypass traditional shelf constraints. Peppersmith, priced at GBP 15.99 to GBP 19.99 for multi-packs, offers subscription discounts and highlights its Oral Health Foundation endorsement in digital campaigns, turning educational content into recurring revenue. Similarly, PUR Company increased U.S. sales by 80.6% to USD 8.6 million in the 52 weeks ending May 2025, leveraging its Amazon presence and allergen-free positioning to appeal to parents buying for children. In China, live-streaming and influencer partnerships are helping niche sugar-free gum brands grow in fragmented retail markets. This shift allows emerging brands to scale without large promotional budgets, though profitability depends on managing customer acquisition and retention costs effectively.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, North America held 41.8% of the market share, driven by decades of oral-health marketing, strong retail infrastructure, and high per-capita consumption. However, growth remains limited to low single digits due to market maturity. Mars Wrigley’s 2024 "Chew You Good" campaign repositioned Orbit, Extra, Freedent, and Yida as wellness products, aligning with the demand for low-calorie, mouth-hydrating options linked to GLP-1 medication use. In Canada, Mars Wrigley launched EXCEL Refreshers in July 2024, targeting younger consumers with a soft-chew format. Mexico offers growth potential due to its large population and rising incomes, but price sensitivity challenges premium natural-sweetener products. Regulatory stability in the U.S., with FDA approval of six high-intensity sweeteners, contrasts with WHO’s cautious stance on non-sugar sweeteners, which premium brands leverage by focusing on dental benefits.

Europe maintained a strong market share in 2025, led by Germany, the UK, France, and Spain, supported by oral-health awareness and sugar-free regulations. The European Food Safety Authority reaffirmed sweetener safety in 2024, while Germany’s 2025 guidance on sweetener risks highlighted opportunities for natural-sweetener brands. Peppersmith uses British peppermint oil and Oral Health Foundation endorsements to justify premium pricing. Perfetti Van Melle’s 2023 acquisition of Mondelez’s gum business strengthened its European presence. Smaller markets like the Netherlands and Sweden show high per-capita consumption but limited revenue growth due to population size.

Asia-Pacific is the fastest-growing region, with a 5.98% CAGR forecast through 2031, driven by urbanization, rising incomes, and diabetes awareness. China’s snack market, valued at RMB 1,344.0 billion in 2024, is growing at 5.5% CAGR, with content-driven e-commerce boosting niche sugar-free gum brands. Discount stores in China are growing positively, favoring affordable sugar-free options. India’s confectionery market remains price-sensitive, with sugar-free gum appealing to urban middle-class consumers. Japan’s high per-capita consumption is supported by Lotte’s Xylitol Oratect Gum, which carries a special health-food designation. Mars Wrigley’s USD 33 million investment in Kenya in 2025 highlights confidence in East African demand and a shift toward emerging markets. Australia, Indonesia, South Korea, and Thailand also contribute to regional growth, with Australia showing strong demand for natural-sweetener brands like Epic and PUR.

South America, the Middle East, and Africa held smaller shares in 2025 but showed growth potential due to urbanization and health awareness. Brazil and Argentina lead South American consumption, though economic challenges limit premium product growth. Colombia, Chile, and Peru see rising middle-class demand, but fragmented distribution restricts reach. In the Middle East and Africa, countries like South Africa, Saudi Arabia, and Nigeria show growing interest in sugar-free gum, with growth depending on retail modernization and consumer education. Mars Wrigley’s investment in Kenya reflects optimism for East African demand, focusing on value-priced products to address price sensitivity.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Multinational confectionery giants dominate the sugar-free chewing gum market, holding a substantial share of global sales. These major players leverage their established brand portfolios, robust retail partnerships, and vast distribution networks to secure prime placements in supermarkets, convenience stores, and pharmacies. Their size allows for consistent investments in marketing, product reformulation, and flavor innovation, bolstering brand loyalty and encouraging repeat purchases.

While a few dominant firms lead the market, regional manufacturers and niche brands find their footing through unique positioning. Many of these smaller entities spotlight natural sweeteners, clean-label offerings, or functional advantages like promoting oral health and enhancing cognition. This strategy carves out competitive niches within specific consumer segments, even as overall leadership remains with the larger players.

In mature markets, where retail space is at a premium and impulse buying reigns, competitive dynamics hinge on pricing tactics, promotional efforts, and negotiations for shelf space. Established firms enjoy advantages from entry barriers like brand recognition, regulatory hurdles, and distribution channels. Yet, emerging brands are making inroads, especially by appealing to health-conscious and premium market segments. This interplay results in a market that's moderately consolidated, blending the dominance of larger players with the innovative spirit of niche competitors.

Sugar-free Chewing Gum Industry Leaders

-

Ferrero International SA

-

Mars Incorporated

-

Mondelēz International Inc.

-

Perfetti Van Melle BV

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Mars Wrigley has launched local production of sugar-free Orbit and Extra chewing gum in Kenya, following a USD 33 million investment in their Athi River plant. This expansion aims to boost supply chain resilience, reduce reliance on European imports, and serve the African and Middle East markets.

- May 2025: Trident Vibes introduced the only sugar-free Cotton Candy flavored gum. According to the brand, the gum contains 35% fewer calories than sugared gum. This sugarless gum has only 5 calories per piece and is coated with a crunchy candy-like shell that’s packed with the irresistible sweet treat flavor of cotton candy.

- March 2025: Wrigley Extra, one of the leading chewing gum brands, partnered with dental professionals around the world to promote the use of sugar-free chewing gum to improve oral health. The brand’s Wrigley Oral Health Program states that: “Gum base puts the 'chew' in chewing gum, binding all the ingredients together for a smooth, soft texture.

Global Sugar-free Chewing Gum Market Report Scope

Sugar-free chewing gum is a type of chewing gum formulated without added sucrose or other traditional sugars. Instead, it uses alternative sweeteners such as sugar alcohols (e.g., sorbitol, xylitol, maltitol) or high-intensity sweeteners (e.g., aspartame, sucralose, stevia) to provide sweetness while delivering reduced or zero sugar content. The Sugar-Free Chewing Gum Market Segments by Form into Stick Gum, Dragee Gum, Tablet, Soft Chew/Cubes, and Others. Sweetener Types are divided into Natural and Artificial Sweeteners. Distribution Channels include Supermarket/Hypermarket, Online Retail Store, Convenience Store, and Others. Geographically, the market spans North America, Europe, Asia-Pacific, South America, the Middle East and Africa. Market Forecasts are Presented in USD Value Terms.

Form

| Stick Gum |

| Dragee Gum |

| Tablet |

| Soft Chew / Cubes |

| Others |

Sweetener type

| Natural Sweeteners |

| Artificial Sweeteners |

Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Form | Stick Gum | |

| Dragee Gum | ||

| Tablet | ||

| Soft Chew / Cubes | ||

| Others | ||

| Sweetener type | Natural Sweeteners | |

| Artificial Sweeteners | ||

| Distribution Channel | Supermarket/Hypermarket | |

| Online Retail Store | ||

| Convenience Store | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF