Polyester Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

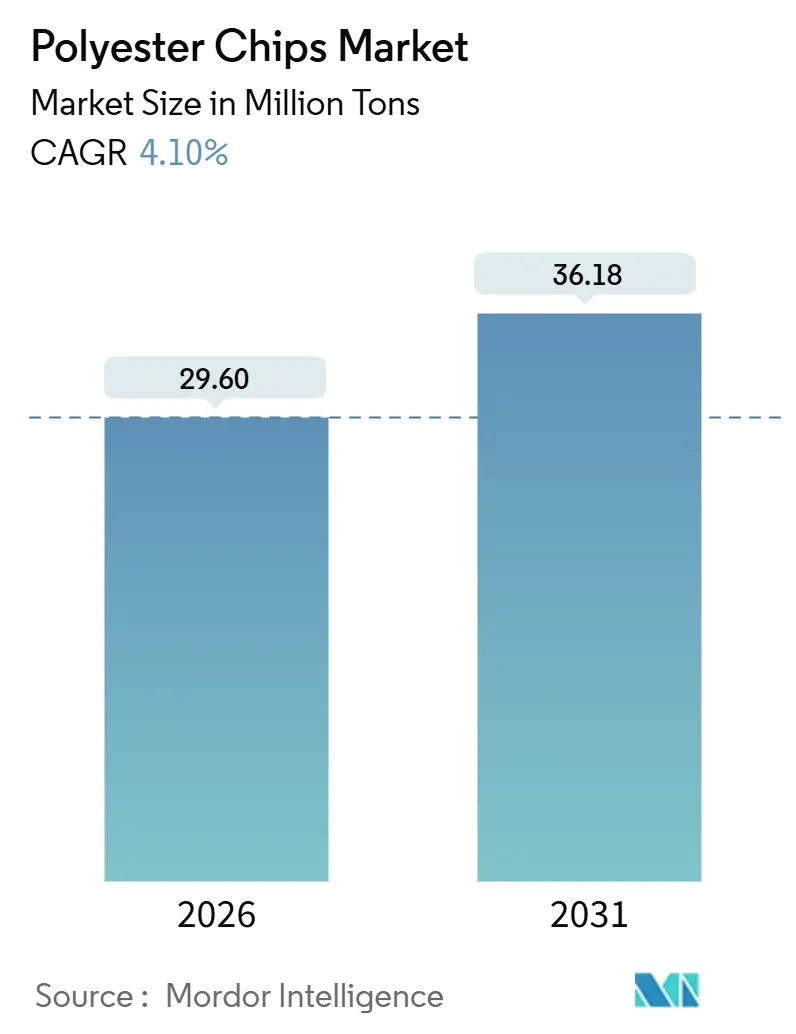

| Market Volume (2026) | 29.60 Million tons |

| Market Volume (2031) | 36.18 Million tons |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyester Chips Market Analysis by Mordor Intelligence

The Polyester Chips Market size is estimated at 29.60 million tons in 2026, and is expected to reach 36.18 million tons by 2031, at a CAGR of 4.10% during the forecast period (2026-2031). Fibers, bottles, and films each respond differently to tightening circular-economy rules, chronic Asian overcapacity, and brand-level sustainability pledges. OECD regulations that set minimum recycled-content thresholds continue to stimulate demand for food-contact rPET, while the cost advantage enjoyed by feedstock-integrated facilities in China and the Middle East pressures margins elsewhere. Top-ten Chinese producers already control a significant portion of domestic output. Meanwhile, premium pricing for chemically recycled resin in Europe and North America helps offset higher carbon costs, encouraging converters to secure long-term offtake agreements. These cross-currents collectively temper virgin-resin growth and sharpen the focus on mechanical and chemical recycling capacity that can satisfy brand mandates.

Key Report Takeaways

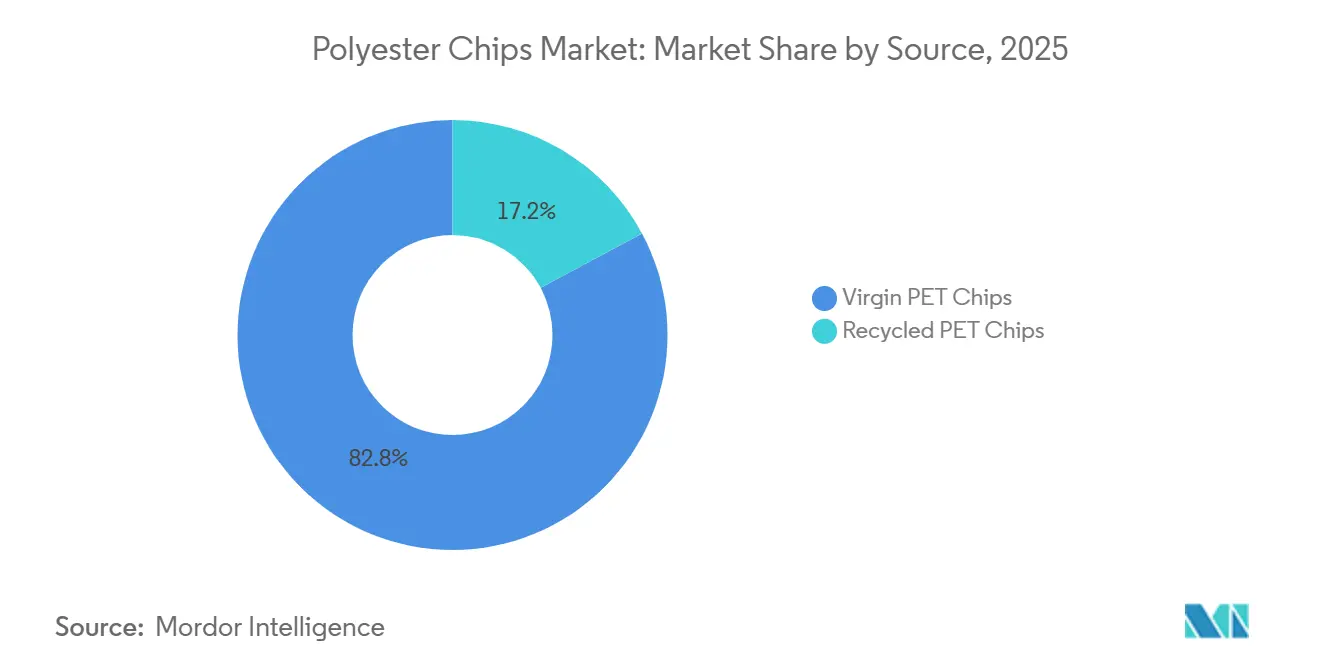

- By source, virgin PET held 82.83% of the 2025 volume, whereas recycled PET recorded the fastest 4.27% CAGR toward 2031.

- By grade, fiber-grade chips captured 50.90% of 2025 volume and are forecast to lead growth at a 4.37% CAGR through 2031.

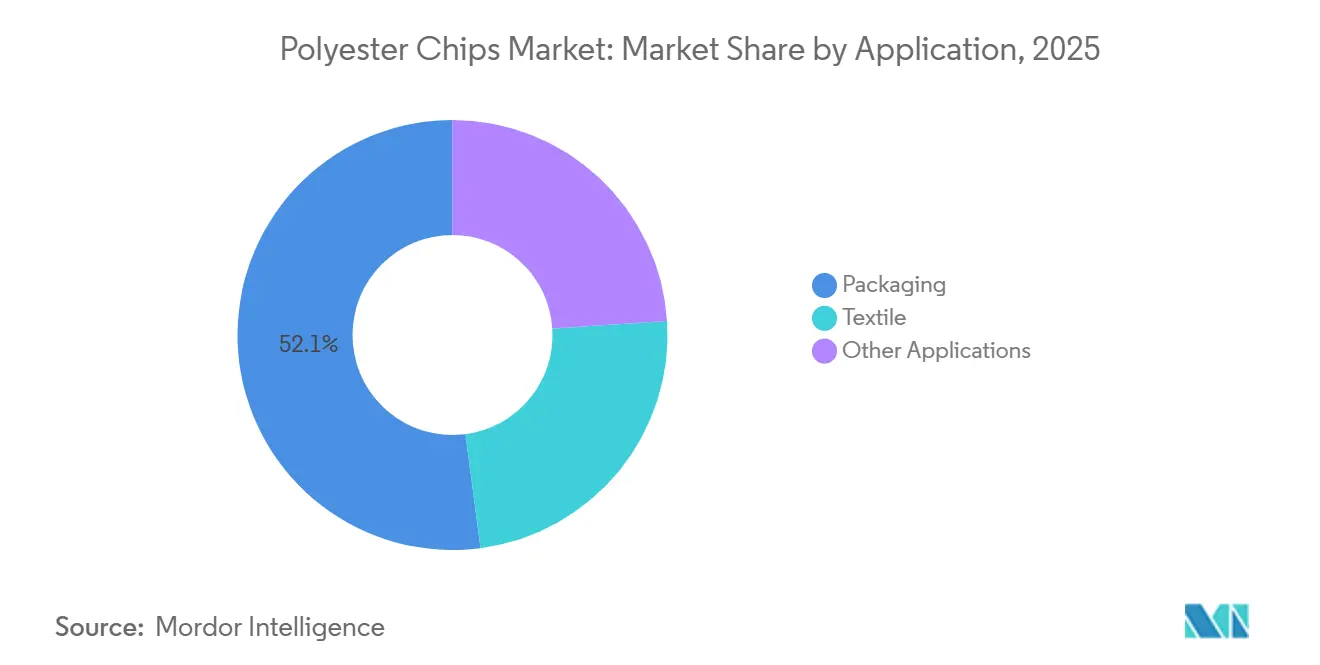

- By application, packaging commanded 52.08% of 2025 demand and is expected to log the quickest 4.37% CAGR over the outlook.

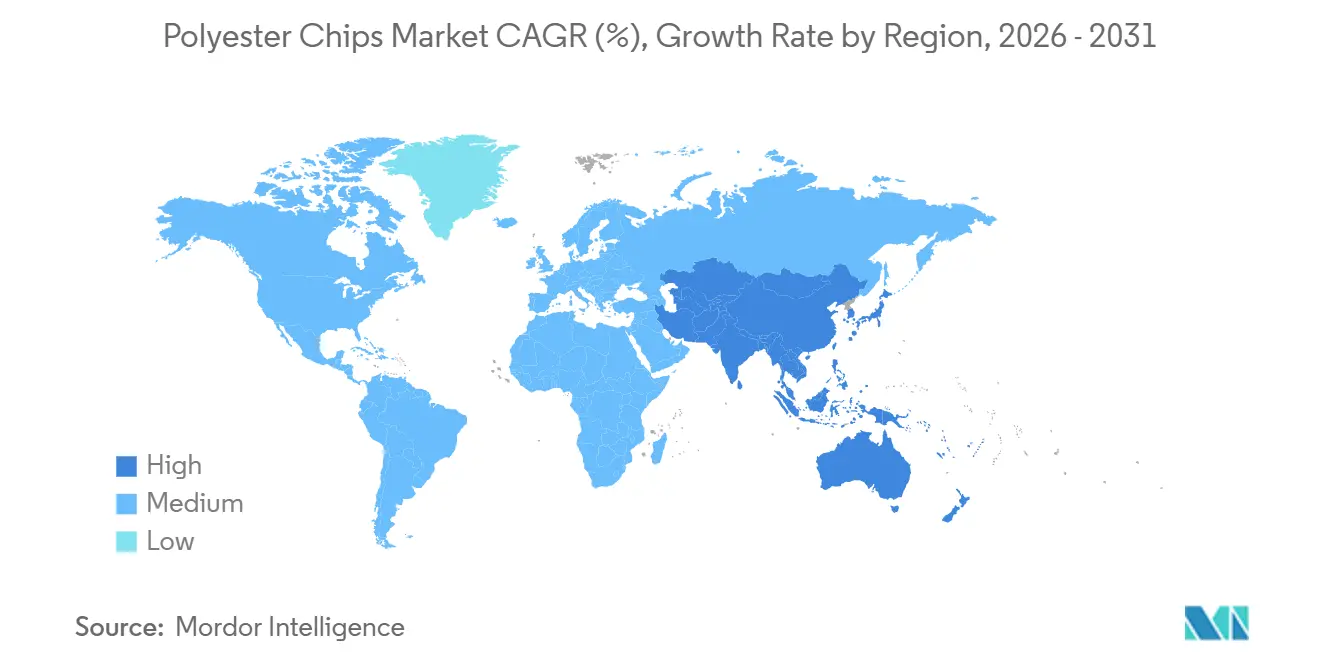

- By geography, Asia-Pacific secured 54.98% of the polyester chips market share in 2025 and is on track for a 4.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyester Chips Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on sustainability and recycled-content mandates | +1.2% | Global, with regulatory leadership in EU, California, and brand-driven adoption in North America and Asia | Medium term (2-4 years) |

| PET cost competitiveness and vertical-integration economics | +0.9% | Middle East, China, India (feedstock-advantaged regions) | Long term (≥ 4 years) |

| Rising demand from textile and PSF sector in emerging Asia | +1.0% | India, Vietnam, Bangladesh, Indonesia | Medium term (2-4 years) |

| Brand-level rPET sourcing commitments accelerating chemical recycling | +0.8% | Global, concentrated in North America and Europe for brand headquarters; production in Asia | Medium term (2-4 years) |

| Surge in bottle-to-bottle capacity in MEA and LatAm via circular-economy laws | +0.5% | Middle East (Saudi Arabia, UAE), Latin America (Brazil, Mexico), South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Sustainability and Recycled-Content Mandates

Governments are turning concerns about plastic waste into binding quotas, boosting the demand for recycled feedstock. For example, the EU's Single-Use Plastics Directive mandates that beverage bottles contain recycled PET (rPET) by 2025 and by 2030[1]European Commission, “Single-Use Plastics Directive 2019/904,” ec.europa.eu. Similarly, California's Senate Bill 54 sets a target of rPET by 2030. Currently, mechanical recyclers provide only a limited amount annually, falling short of the amount promised by brands. As a result, chemical depolymerization methods are rapidly expanding. Carbios launched its enzymatic-recycling plant in Longlaville in 2025, securing partnerships with L’Oréal, Nestlé Waters, and PepsiCo[2]Carbios, “Longlaville Enzymatic Recycling Plant Commissioning,” carbios.com. Eastman Chemical's facilities in Kingsport and Normandy, utilizing methanolysis, contribute additional chemically recycled capacity. This expansion highlights the widening gap between converters meeting regulations and those lagging behind. Under Regulation 2022/1616, recyclers must pass challenge tests and disclose non-intentionally added substances. This regulation raises the compliance standards for mechanical operations, giving an edge to advanced technologies. Given that food-contact rPET fetches a premium over virgin materials, converters are increasingly securing long-term supply contracts. This trend solidifies recycled resin's role as a key growth driver for the polyester chips market.

PET Cost Competitiveness and Vertical-Integration Economics

Backward-integrated complexes shield producers from fluctuations in crude oil prices and the volatility of PTA/MEG spot prices. Hengli Group operates a crude-to-chemicals complex in Dalian, directly converting refinery streams into paraxylene and PTA. This integration allows Hengli to maintain lower cash costs compared to its non-integrated competitors. In the Middle East, Saudi Aramco and SABIC utilize low-cost naphtha to produce ethylene glycol. This cost advantage enables them to ship virgin chips at prices that undercut European offers, even after accounting for freight and duties. However, the EU's Carbon Border Adjustment Mechanism, which has been monitoring since 2023 and is set to impose tariffs starting in 2026, could increase the cost of Middle Eastern polymer imports once plastics are factored in. As a result, integrated producers are now evaluating their long-term capital expenditures in light of these impending trade challenges. This scrutiny is driving them to diversify towards circular feedstocks and bio-based methods, which boast lower embedded emissions. Such strategic moves bolster the position of these cost-advantaged giants, while simultaneously putting pressure on standalone converters in the polyester chips market.

Rising Demand from Textile and PSF Sector in Emerging Asia

India's textile economy is set to grow significantly by 2030. Under the Production Linked Incentive scheme, the Indian government has allocated substantial funds to bolster man-made fiber capacity. This initiative is poised to elevate domestic polyester filament output over the coming years. Meanwhile, authorities in Vietnam are championing a large-scale rPET complex in Nghi Son, eyeing a start-up in late 2026. Bangladesh, with its sights set on substantial growth in ready-made garment exports by 2030, is witnessing a surge in demand for wrinkle-resistant polyester fabrics. As synthetic fibers dominate, accounting for a significant share of global production, Asian mills are emerging as the primary destination for fiber-grade chips. This robust demand in textiles is counterbalancing certain regulatory challenges in packaging, ensuring the polyester chips market remains closely aligned with apparel demand cycles.

Brand-Level rPET Sourcing Commitments Accelerating Chemical Recycling

Consumer-goods companies are now turning corporate sustainability pledges into enforceable procurement contracts. Coca-Cola aims for 50% recycled PET (rPET) in all its plastic packaging by 2030. PepsiCo is aligning with this goal, while Unilever is setting its sights on 25% recycled plastic by 2025. Loop Industries has struck a deal, licensing its Infinite Loop technology to SK Chemicals. Additionally, in collaboration with Ester Industries, Loop is building a plant in India, targeting operational readiness by 2027. Indorama Ventures, having already recycled a significant number of bottles, is ambitiously targeting increased rPET capacity by the close of 2025. With branded demand for food-contact rPET exceeding current supply, chemical-recycling offtake agreements are increasingly being used as anchor contracts. These agreements not only mitigate risks associated with capital deployment but also bolster the recycled segment of the polyester chips market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic over-capacity and price competition | -0.8% | China, South Korea, Europe (non-integrated producers) | Short term (≤ 2 years) |

| Single-use-plastic regulations and reusable-packaging shift | -0.4% | EU, India, Canada, select US states | Medium term (2-4 years) |

| Escalating carbon-pricing in OECD nations eroding margins | -0.3% | EU (ETS), potential future CBAM expansion to polymers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Over-Capacity and Price Competition

By the end of 2025, China's polyester capacity had risen, yet had not reached full utilization. In 2023, spot PET prices dipped significantly. While they found stability in 2024, the global landscape revealed a daunting volume of idle assets, pressuring margins. Lotte Chemical significantly reduced its South Korean capacity, Alpek put its Cedar Creek facility in the U.S. on hold, and Plastiverd closed its plant in Spain. These moves underscore the strain on non-integrated, high-cost sites. With the top ten Chinese firms commanding a significant market share, further consolidation appears inevitable. However, demand growth alone will not swiftly absorb the existing surplus capacity, casting a shadow over the polyester chips market.

Single-Use-Plastic Regulations and Reusable-Packaging Shift

India banned 19 single-use plastic items in July 2022, but notably exempted PET bottles. Instead of an outright ban, India imposed Extended Producer Responsibility (EPR) fees on these bottles, effectively internalizing their collection costs. In December 2022, Canada rolled out a similar prohibition, targeting checkout bags, cutlery, and specific food containers, yet bottles remained exempt. Even with PET bottles spared from bans, deposit-return schemes achieving high collection rates have curtailed the demand for virgin materials, as recycled PET (rPET) increasingly replaces prime resin. Beverage industry leaders are experimenting with refill stations and concentrated pouches, which utilize fewer bottles per occasion. This trend suggests a potential cap on the future demand for virgin materials, especially in packaging. As a result, the polyester chips market is leaning more on the textile and film sectors to balance out the anticipated stagnation in packaging demand.

Segment Analysis

By Source: Recycled Resin Closes the Gap With Virgin

Virgin grades still account for the bulk of material, but recycled output is advancing at the fastest clip. In 2025, virgin comprised 82.83% of the supply, yet recycled volume is registering a 4.27% CAGR to 2031. Mechanical recyclers, including Indorama Ventures, Filatex India, and Ester Industries, collectively boosted their rPET capacity during 2025-26. Chemical processes are not lagging; Carbios, Eastman, and Loop Industries are set to contribute additional advanced-recycled output by 2027. While persistent over-capacity in virgin materials keeps prime resin prices low for textiles, brand-driven premiums for food-grade rPET are fueling swift investments. Consequently, the share of the polyester chips market allocated to recycled streams is poised to double by the early 2030s.

Emerging chemical methods are pivotal for food-contact compliance. Regulation 2022/1616 mandates stringent challenge tests, a hurdle that enzymatic and methanolysis plants are engineered to overcome. As a result, mechanical lines are increasingly focusing on textiles and non-food packaging, while chemical depolymerizers target bottle applications. Indorama adopts a dual-route strategy, while newcomers like SK Chemicals are leaning towards licensing platforms such as Infinite Loop, ensuring virgin-equivalent purity from the outset. Thus, securing brand contracts emerges as a crucial element in monetizing new rPET assets, significantly influencing the competitive dynamics of the polyester chips market.

By Grade: Fiber-Grade Dominates, Bottle-Grade Sets the Price Tone

Fiber-grade chips represented 50.90% of 2025 demand and are poised to grow 4.37% annually through 2031. This growth is a testament to the ongoing expansion of the textile industry in South and Southeast Asia. Notably, India is making significant strides with plans for seven PM MITRA parks. These parks, designed for integrated polyester mills, come with bundled incentives like land, power, and logistics. As a result, local consumption is projected to surge substantially by 2030. Meanwhile, neighboring countries like Bangladesh and Vietnam are on parallel paths, actively sourcing both virgin and recycled chips for their yarn-spinning industries. Furthermore, given that fiber applications can accommodate intrinsic viscosities ranging from 0.60 to 0.70 dL/g, there's a strong market for lower-grade mechanical rPET, bolstering the economics of recycling.

While bottle-grade chips command a smaller volume in the market, they wield significant influence over price trends. Supply constraints arise from stringent food-contact specifications and acetaldehyde limits. These challenges are magnified with the impending recycled-content mandates set to be enforced in the EU and select regions of the U.S. Forecasts indicate that the market size for bottle-grade rPET polyester chips will grow significantly by 2031, marking it as the segment with the steepest growth trajectory. Producers of mechanically and chemically recycled chips enjoy a premium over their virgin counterparts, ensuring healthy profit margins. A new elite tier of bottle-grade suppliers has emerged, adept at navigating stringent purity regulations. This group includes Indorama's expansive global network, Eastman's state-of-the-art plants in the U.S. and France, and Carbios' innovative enzymatic approach.

Film-grade chips, though occupying a smaller segment of the market, are witnessing rapid growth, primarily driven by demand in flexible packaging and photovoltaic installations. Origin Materials is making a strategic move into this burgeoning market with its bio-attributed resin, boasting a significant capacity set to come online by 2027. Concurrently, producers in China are aggressively expanding, launching new stretch-film lines specifically designed for solar backsheets. While film applications currently represent less than ten percent of the overall polyester chips market, their technical requirements command above-average profit margins, making them a hotspot for specialty-grade innovations.

By Application: Packaging and Textiles Run Neck-and-Neck

Packaging made up 52.08% of demand in 2025 and is forecast for a 4.37% CAGR to 2031. Bottle applications constitute the lion’s share, anchored by Coca-Cola, PepsiCo and Nestlé Waters commitments. Rigid-tray and thermoform grades lag slightly because food-contact clearance for recycled content is harder to gain, but ongoing EFSA approvals are unlocking incremental opportunities. Deposit-return systems in Germany and Norway uplift collection rates, feeding high-quality flake back to bottle lines and effectively closing the loop within the polyester chips market.

Textiles almost match packaging’s growth. Performance apparel brands prioritize recycled polyester, and Nike, Adidas, and Decathlon collectively contract several hundred thousand tons of rPET annually. Fiber-to-fiber chemical recycling, once viewed as distant, edges closer as projects like Evonik-Oerlikon target commercial scale circa-2030. Industrial fabric, home furnishings, and automotive interiors also absorb rising volumes, diversifying end-use risk.

Other applications—engineering resins, strapping, specialty films—provide demand stability. Because these segments demand mechanical strength over optical clarity, they absorb virgin grades that might otherwise face oversupply, cushioning overall volatility in the polyester chips market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific, in 2025, the region held 54.98% of global volume, and its 4.65% CAGR keeps it firmly atop the regional ranking through 2031. China, a powerhouse in the PET arena, boasts nearly half of the world's PET capacity. Meanwhile, India, spurred by PLI incentives and a surge in garment exports, stands out as the most promising demand center. Even as domestic polymerization ramps up, India continues to pull in imports. Further underscoring the region's growing appetite are Vietnam’s Nghi Son rPET project and Bangladesh’s expansion in ready-made garments.

Europe and North America find themselves in a state of flux. In Europe, the EU ETS costs challenge the competitiveness of virgin materials. Yet, with mandates for rPET, there's a guaranteed demand for premium recycled chips. The momentum for local chemical recycling is evident with Carbios’ and Eastman’s plants in France. Alpek’s decision to restart operations in the U.K. hints at a positive shift in regional utilization rates. Across the Atlantic, North America enjoys a bounty of PET bottle feedstock. Additionally, rPET imports from Mexico bolster the U.S. supply, particularly benefiting the West Coast.

South America, the Middle-East, and Africa complete the global picture. Brazil boasts a commendable collection rate, while Mexico rolls out its EPR initiative. South Africa's PETCO success story further strengthens the case for bottle-to-bottle investments, reducing reliance on virgin imports. In the Gulf, while there's a strategic advantage in low-cost feedstock for virgin resin, there's a growing focus on circular projects. This shift aims to ensure continued market access, especially in light of tightening CBAM regulations.

Competitive Landscape

The polyester chips market is moderately consolidated. Strategic moves echo three themes. First, backward integration remains essential for cost leadership, seen in Hengli’s crude-to-chemicals complex and SINOPEC’s refinery-linked PTA units. Second, forward integration into recycling hedges against virgin-demand erosion. Third, geographic diversification spreads regulatory risk: Saudi producers eye Southeast Asia, while Chinese majors explore U.S. and EU recycling joint ventures despite trade headwinds. In this milieu, scale, integration depth, and access to certified rPET feedstock distinguish leaders within the polyester chips market.

Polyester Chips Industry Leaders

Indorama Ventures Public Company Limited

Hengli Group Co., Ltd.

Tongkun Holding Group Co., Ltd.

Far Eastern Group

Alpek S.A.B. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Indorama Ventures Public Company Limited, bolstered by over 20 recycling plants across 11 countries, announced the recycling of its 150 billionth PET bottle, solidifying its leadership in food-grade rPET chips.

- August 2025: Reliance Industries Limited announced to bolster its virgin bottle-grade and fiber-grade PET chips production with a 1 MMTPA specialty polyester expansion, integrated with a 3 MMTPA PTA capacity, targeting commissioning in 2026-27.

Global Polyester Chips Market Report Scope

Polyester (PET) chips are thermoplastic granules derived from the polymerization of PTA and MEG. They are utilized as raw materials for producing fibers, bottles, and films. These chips are categorized into virgin chips (pure polymer) and recycled chips (rPET) and are further graded by viscosity and application into Fiber grade (for textiles), Bottle grade (for packaging), and Film grade (for thin sheets).

The polyester chips market is segmented by source, grade, and application. By source, the market is segmented into virgin PET chips and recycled PET chips. By grade, the market is segmented into fiber-grade polyester chips, bottle-grade polyester chips, and film-grade polyester chips. By application, the market is segmented into packaging, textile, and other applications. The report also covers the market size and forecasts in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

| Virgin PET Chips |

| Recycled PET Chips |

| Fiber-Grade Polyester Chips |

| Bottle-Grade Polyester Chips |

| Film-Grade Polyester Chips |

| Packaging | Bottles |

| Food Packaging | |

| Other Packaging | |

| Textile | |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Source | Virgin PET Chips | |

| Recycled PET Chips | ||

| By Grade | Fiber-Grade Polyester Chips | |

| Bottle-Grade Polyester Chips | ||

| Film-Grade Polyester Chips | ||

| By Application | Packaging | Bottles |

| Food Packaging | ||

| Other Packaging | ||

| Textile | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the polyester chips market in 2026?

The polyester chips market size reached 29.60 million tons in 2026 and is set to climb to 36.18 million tons by 2031, registering a CAGR of 4.10%.

Which region dominates polyester chip consumption?

Asia-Pacific leads with 54.98% volume and a 4.65% CAGR, driven by Chinese capacity and South Asian textile expansion.

What is driving demand for recycled PET chips?

Mandatory recycled-content targets in the EU and U.S., plus brand pledges for 50% rPET bottles, underpin rapid growth in recycled supply.

Why are bottle-grade chips more expensive than fiber-grade?

Food-contact purity standards, intrinsic viscosity requirements, and limited high-quality rPET supply create a premium for bottle-grade material.

How will carbon pricing affect virgin PET production?

EU ETS costs add a premium, eroding European competitiveness and redirecting investment toward low-carbon and recycled routes.